Director’s thoughtpiece: The Challenges This Country Faces

Our beloved NZ has serious challenges; we are not faring as well as other small countries… we may well be at a critical inflexion point. As property investors it is important to understand the key issues, the likely future coalition structure on both sides of the spectrum, how each of them might deal with the issues…and then…the likely impact on property values and cashflows.

To our mind the areas of challenge can be categorised into 5 main areas:

- Finance

- Housing

- Social

- Cost of Living

- Government income/ cost & infrastructure

Below we detail the challenges as we see them. Next Wednesday (23rd August 2023) at our webinar, we will outline how each likely coalition plans to tackle these challenges, and then…the possible impact on property values.

Finance

- Bank reluctance – banks are nervous and thus it is harder to get money out of them. They would say that they want to lend, but their hands are tied if people don’t meet servicing criteria. True, but the bank sets credit criteria. A lift in confidence amongst bank credit teams would see the purse strings loosen…in my humble opinion. If it is hard for people to get finance then they can’t buy, and then developers/ builders don’t have enough demand to get bank finance.

- RBNZ – minimum deposit has eased to 35% for investors. It will be helping – but it won’t be that helpful until servicing criteria eases, which requires interest rates to drop…and bank confidence to improve.

- Interest rates – will only come back once inflation, both local and imported pulls back to the extent that headline inflation in NZ is tracking back to the RBNZ mandated range.

Housing

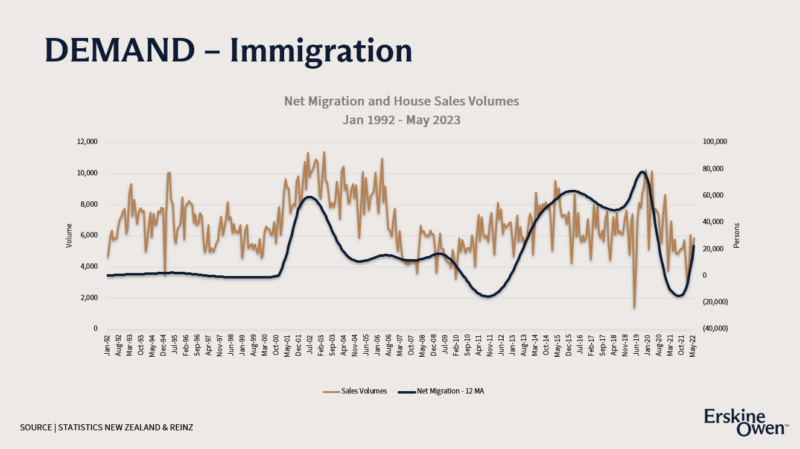

- Demand – has exploded (net migration – see below) back to pre-covid levels and will likely keep going. Growth in population grows demand for housing. Labour hasn’t built the 10,000 homes p.a. it said it would …yet. How will all these people be housed?If you don’t believe me that population growth doesn’t equal demand for housing – have a look at the graph below – a direct correlation.

- Cost of building – it is still very expensive to build. How can builders build if cost of building is greater than what they can sell for? If they can’t build and we need more housing…then what?

- Residential Tenancies Act (RTA) – The last 6 years has seen the residential investment landscape change dramatically. Healthy Homes has largely washed through, and many landlords with plenty of equity decided they’d had enough and cashed up. What has compounded the pressure on landlord cashflow is the price cap during Covid, the restriction on lifting rents to once per annum, and the reduced ability to evict problem tenants. While one of our property managers was walking out of a tribunal hearing recently the mediator told him that they have been instructed not to award termination notices because they can’t handle any more homeless people.

National’s Chris Bishop alleges:

Since 2017, Labour has waged a war on landlords – with the collateral damage borne by tenants. Rents have risen by an average of $175 a week since 2017, the social housing waitlist has quadrupled to more than 23,000 and more than 3000 families live in motels. (source)

- Tax –

- Non deductibility of interest – this is a disincentive to owning residential property.

- Brightline test to 10 years

Cost of Living

- Inflation – it’s still quite high…but is easing.

- Milk prices – break-even price for dairy farmers on milk solids is just under $9 per KG of milk solids. The price has now dropped to between $6.25 and $7.75. That’s a long way off break even. So, a lot of dairy farmers are likely to lose money this year. Tuffley from the ASB thinks it could result in $2b less income for farmers – that is a lot of money taken out of the economy. What will the impact be – what is the forecast for dairy prices?

- Export volumes – Maersk is expecting container volumes to drop, and China import and export growth materially slowing. Chinese exports shrank by 14% in the year to July. David Skilling of Landfall Strategy says this represents an “anaemic Chinese economic recovery”.

- Tourism – its great the borders are back open and that tourists are coming back. But…they are still not at pre-covid levels. That means less spend and less GST and income tax. Why aren’t more people coming to NZ – will they return?

- Red tape – arguably Labour has introduced a lot of red tape…this introduces cost.

Social

Generally, the social fabric of NZ has deteriorated over the last 6 years with school attendance down, crime up and our health system worsening. This can be arguably attributed to Covid; however, commentators would argue that NZ has not done enough post covid to attract investment and stimulate the economy…unlike other countries, e.g., Singapore.

- Immigration – the tap turned off during Covid. The doors are now open to some.

- Health system – Our neighbours go to Thailand every year for health checkups, knowing that if anything serious is found, the quality of facilities and care there is far superior to NZ. OK – so I haven’t been, and they were telling me that over a glass of wine. But you aren’t going to fly Mum, Dad and two kids all that way if it wasn’t better. How does a struggling health system impact the economy and property values?

- Schools – school attendance has declined.

- Crime – ram raids, Auckland downtown shootings. People are tired of it. Is this a driver for some people looking to Aussie? Labour is focussed on ‘well-being’, a big emphasis on the well-being of the offender.

- The great NZ exodus – Perhaps it is just my network – but a lot of people seem to be chatting about moving to Australia. One friend has sold a property and bought a Sydney apartment. OK – so maybe they have a lot more financial independence – but what about the nurses and cops who are being lured to Aus with signing on bonuses, higher salaries, and in some cases better climate.

- Unemployment – Its heading up.

Government/ infrastructure

- Less tax take – Crown revenue is shrinking – no surprise given the economy is slowing. How does a government deal with that when its interest costs have just ballooned?

- NZ Crown debt – Net crown debt up from $6 billion pre pandemic to $71 billion today. This costs the Government – and we pay the Government. How do we pay the interest cost? Should we reduce debt?

- Infrastructure – Lots of stories of potholes on state highways… that may be just the tip of the iceberg. Have we woefully underinvested in our infrastructure? How is that impacting our economy?

- Capital – to build infrastructure NZ needs capital. This government doesn’t necessarily see the wealthy as a ‘friend’.

RSVP below to join us next Wednesday (23rd August 2023) at our webinar, where we will outline how each likely coalition plans to tackle these challenges, and the possible impact on property values.